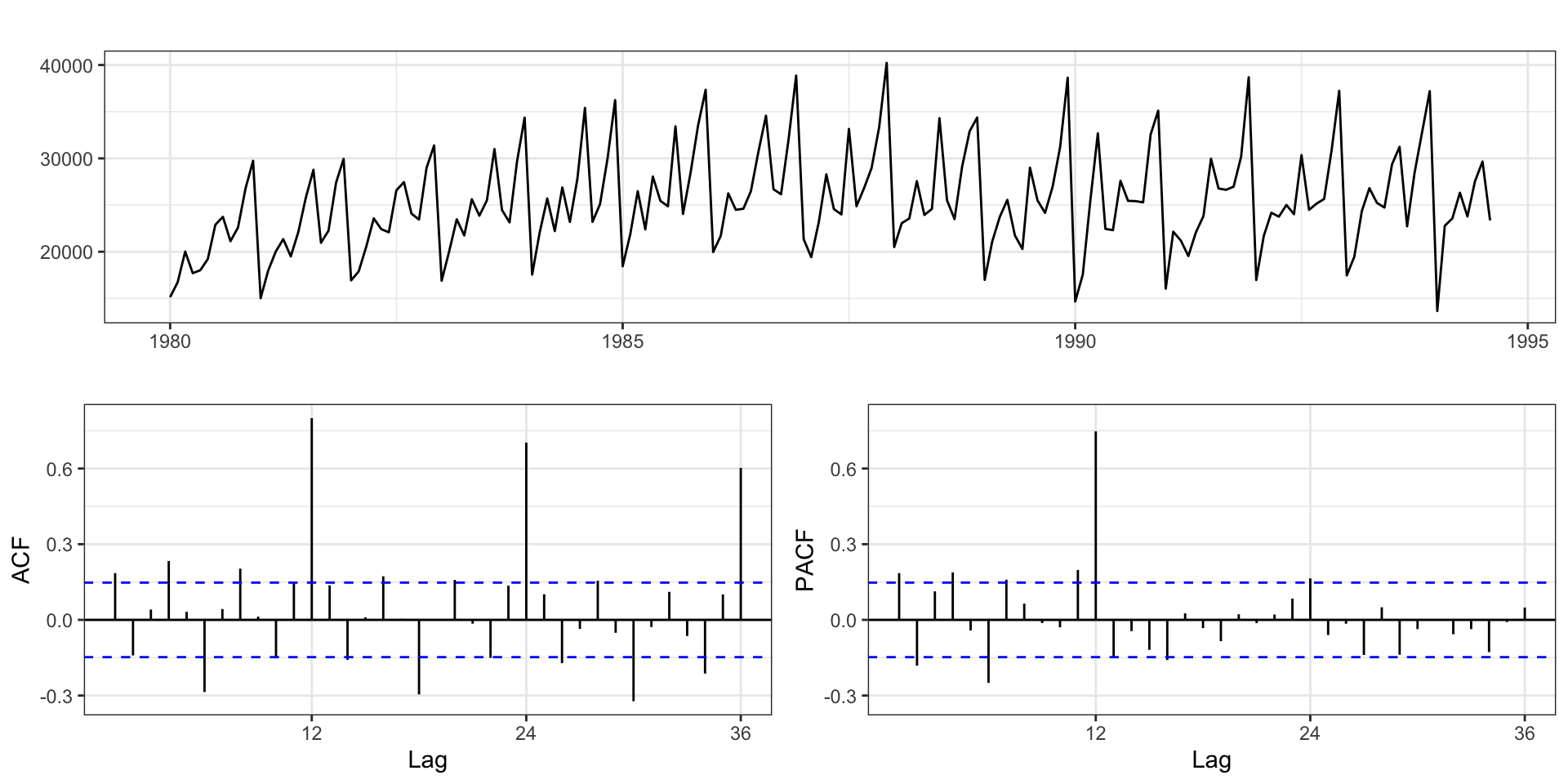

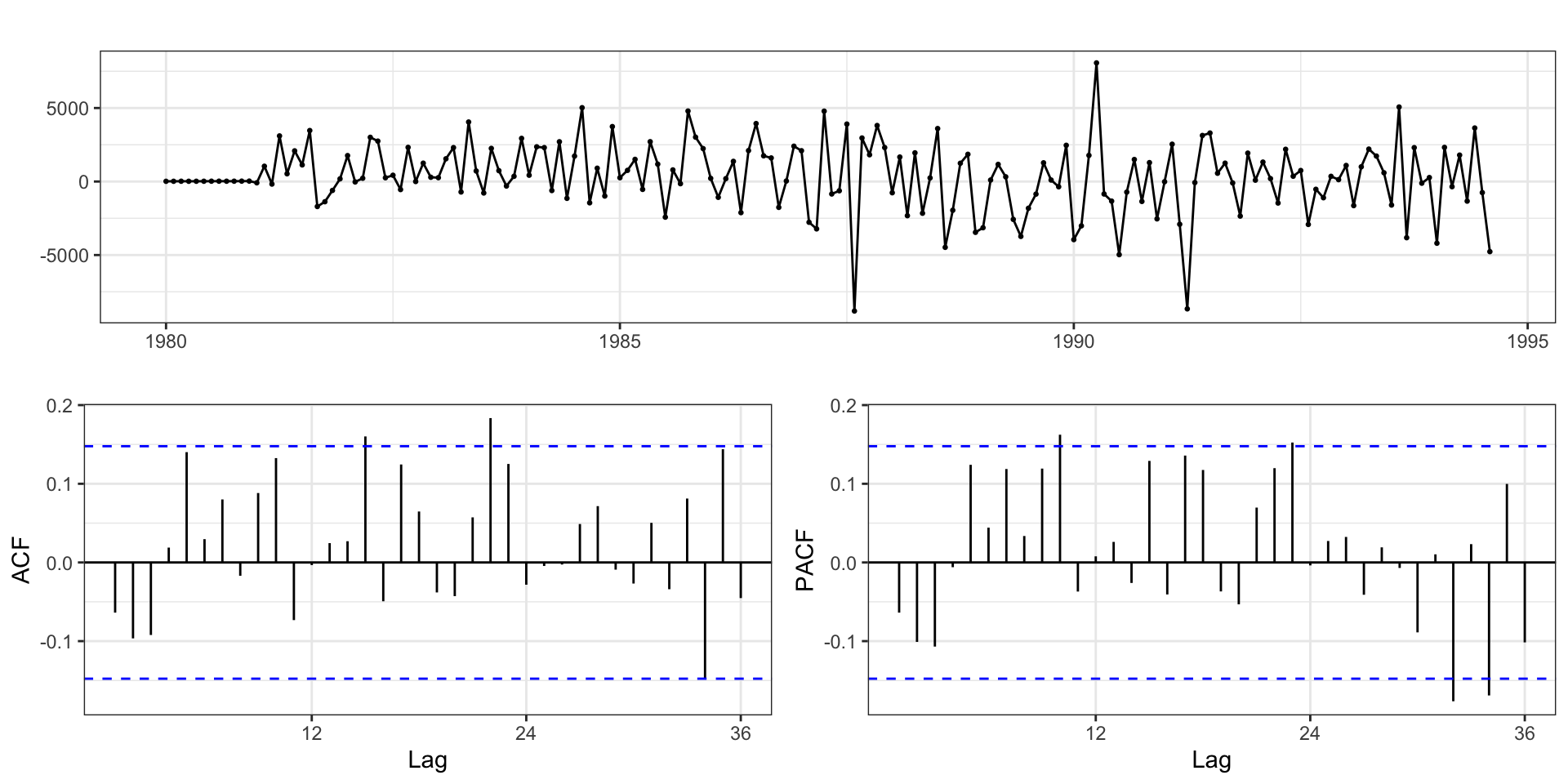

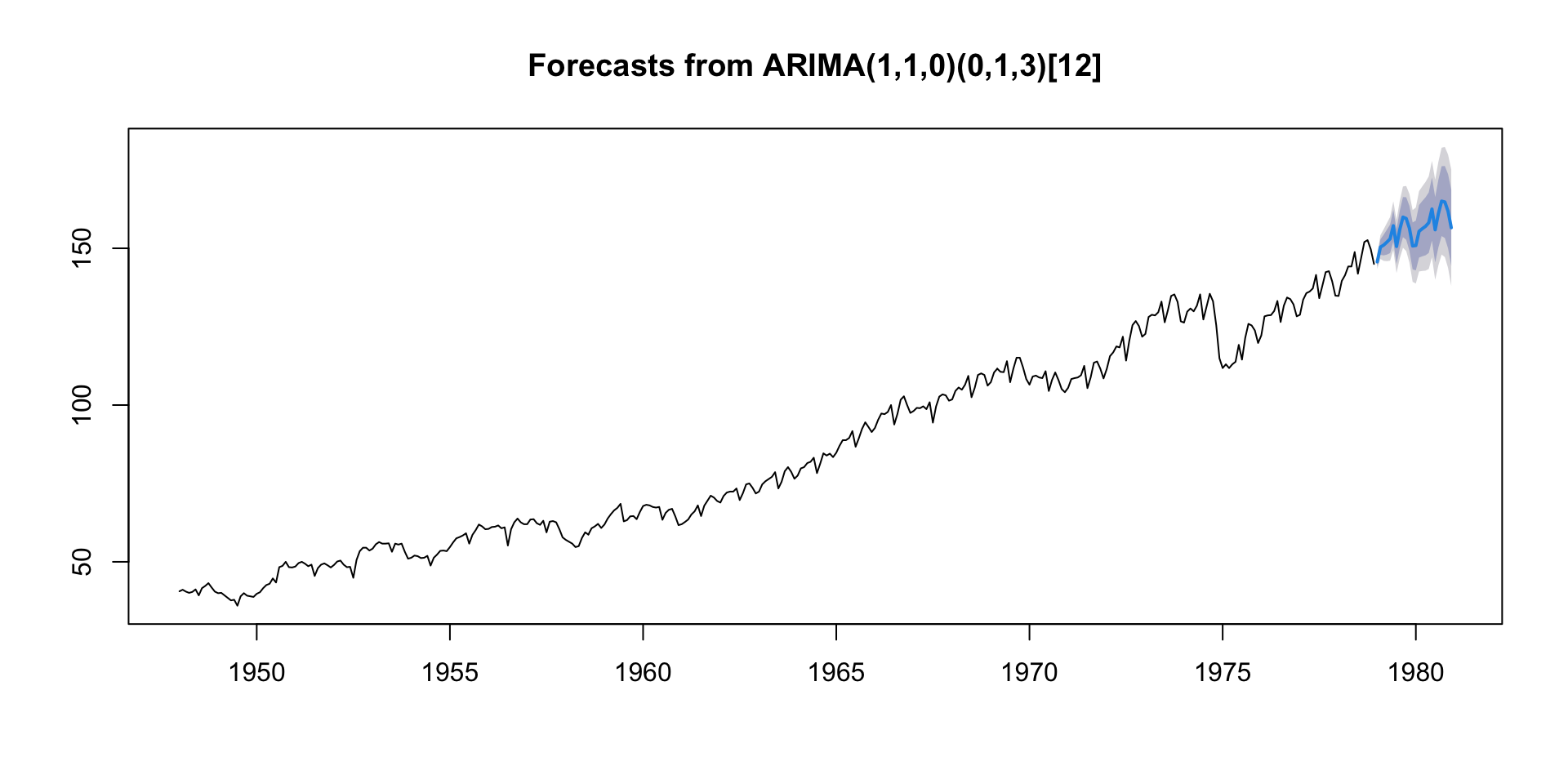

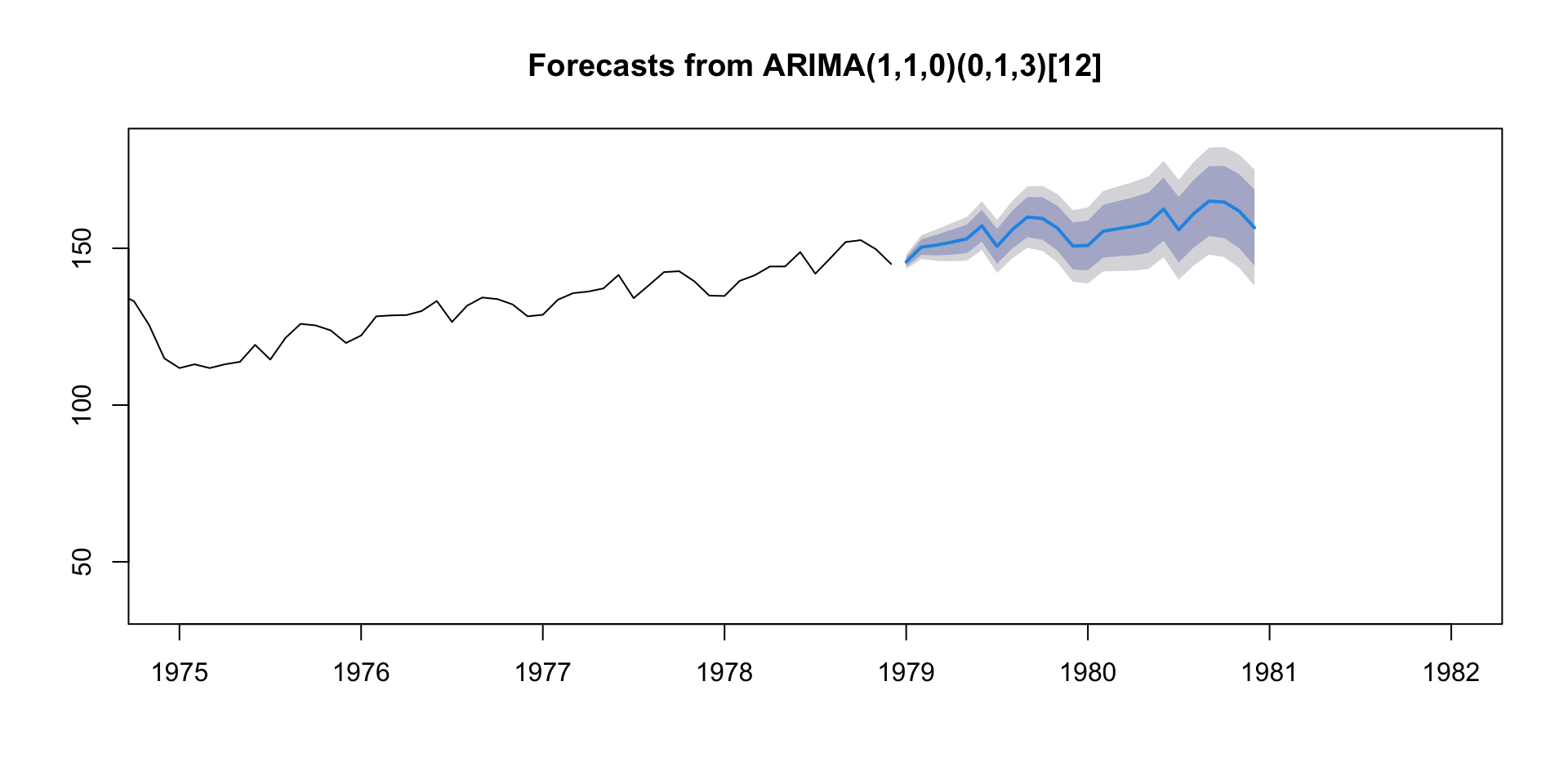

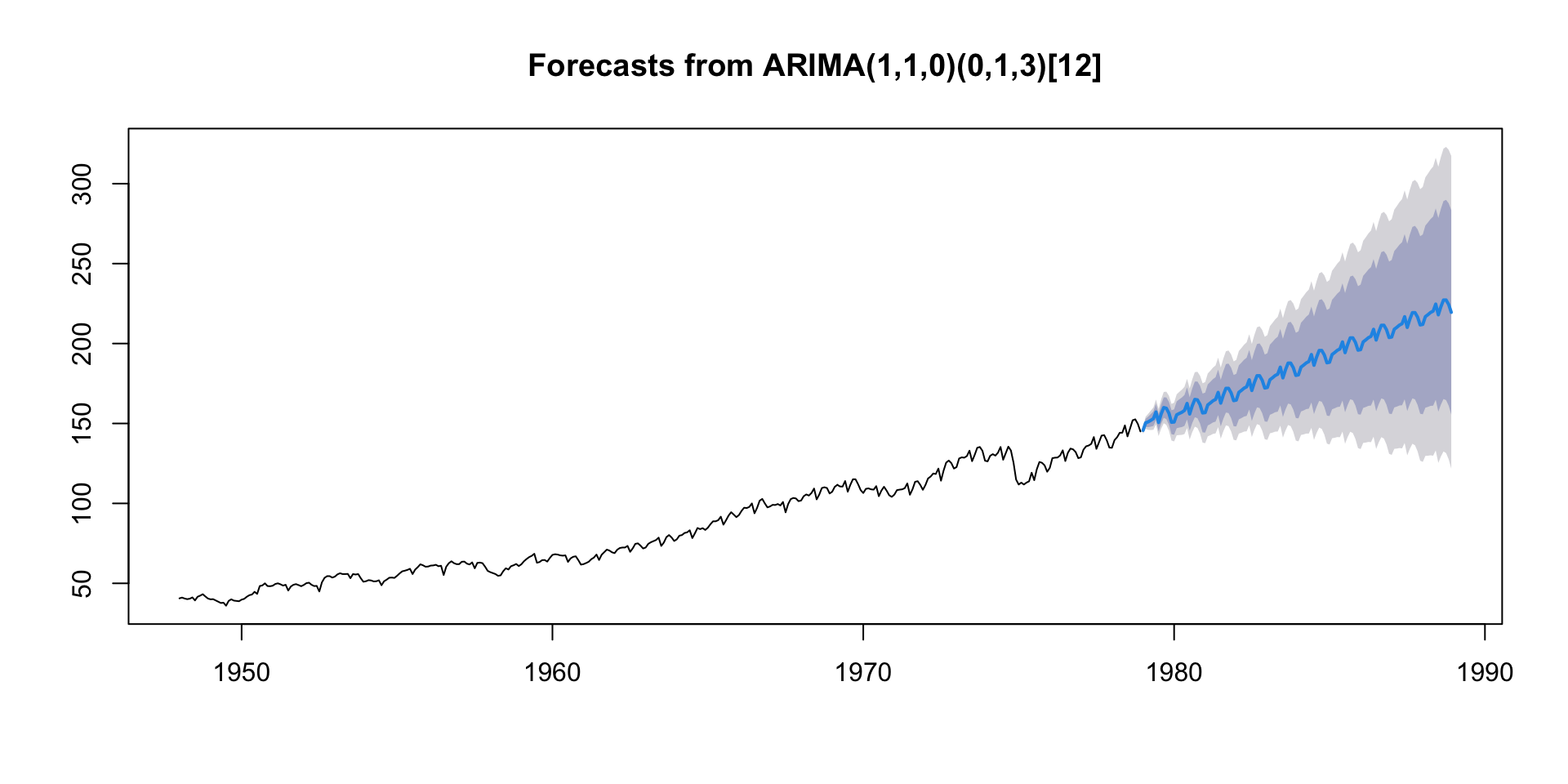

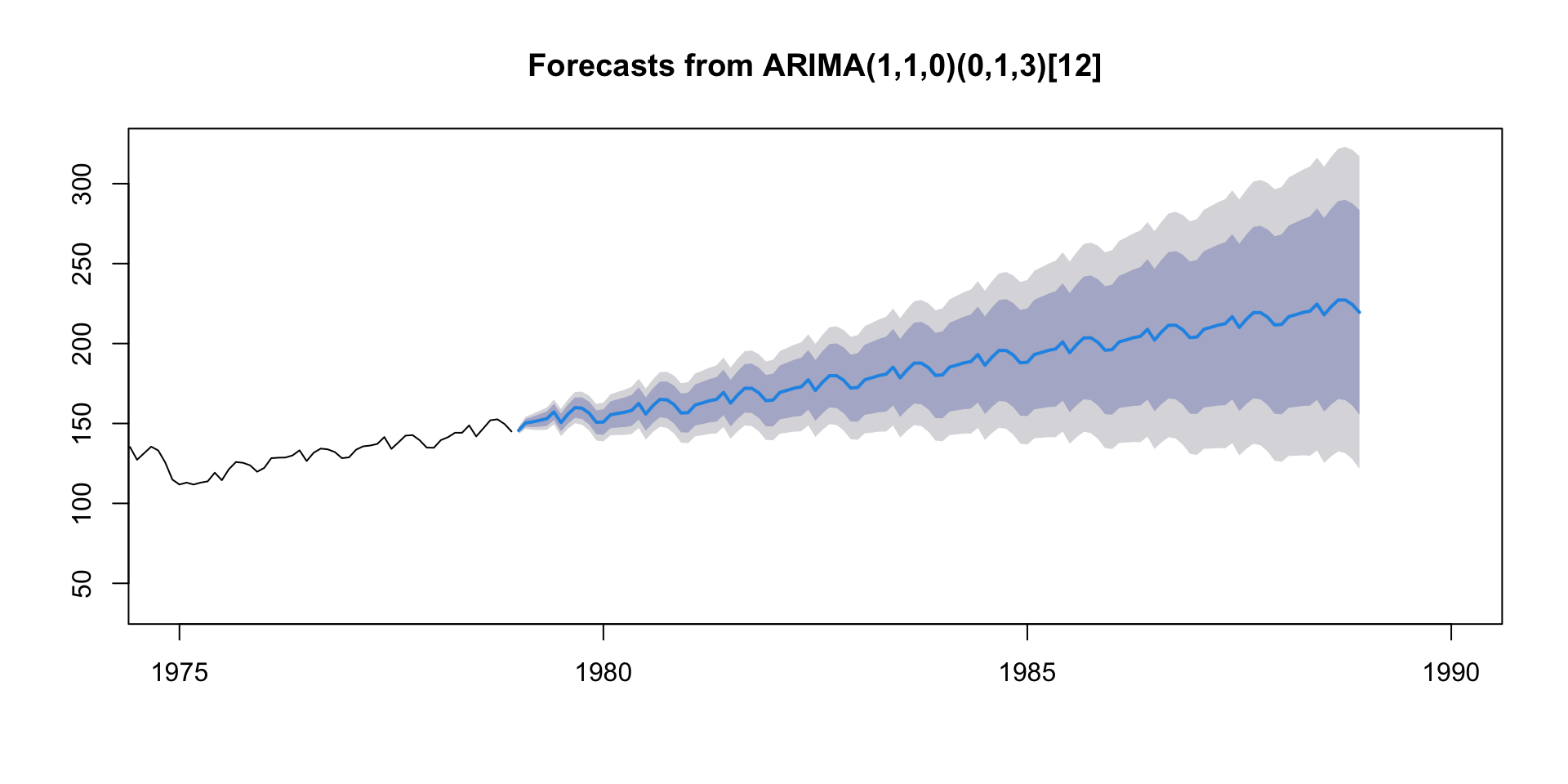

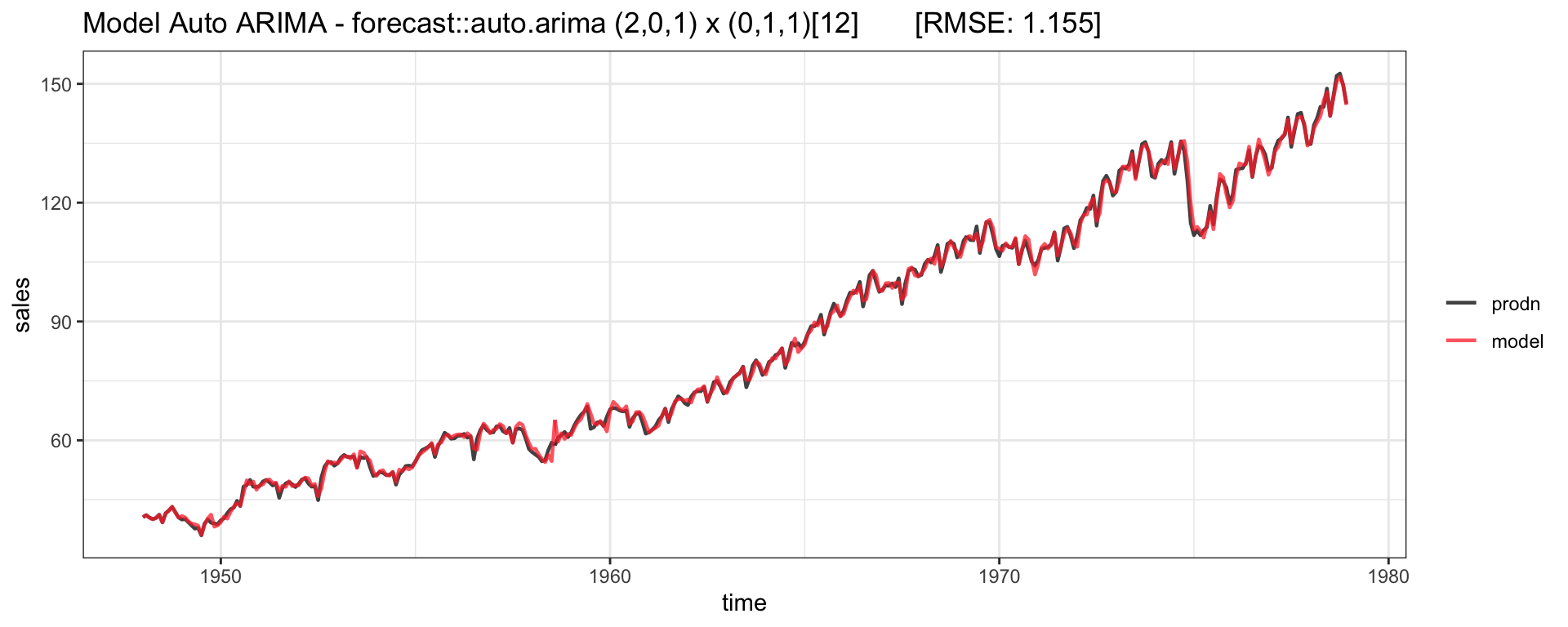

Australian Wine Sales Example

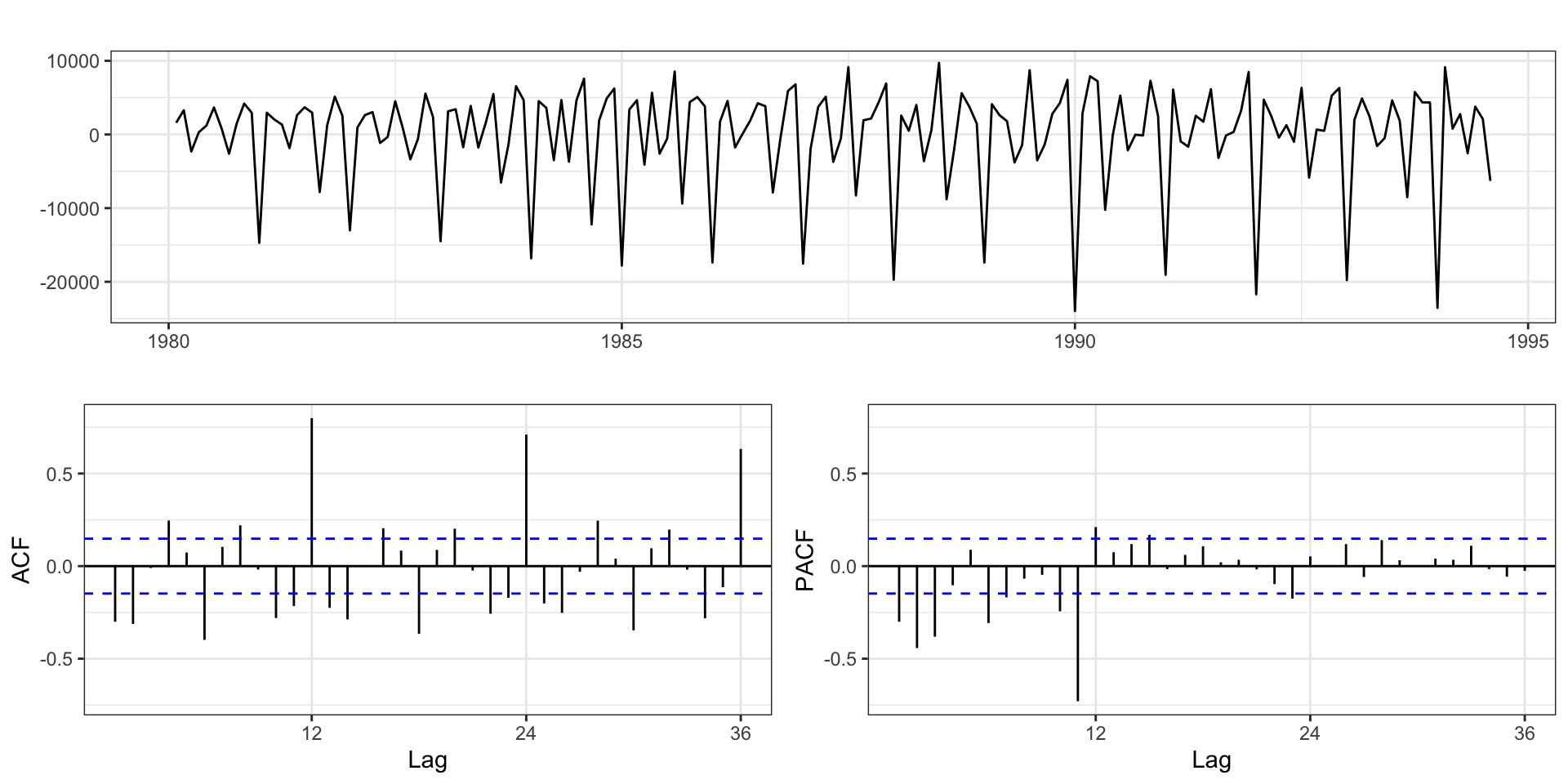

Australian total wine sales by wine makers in bottles <= 1 litre. Jan 1980 – Aug 1994.

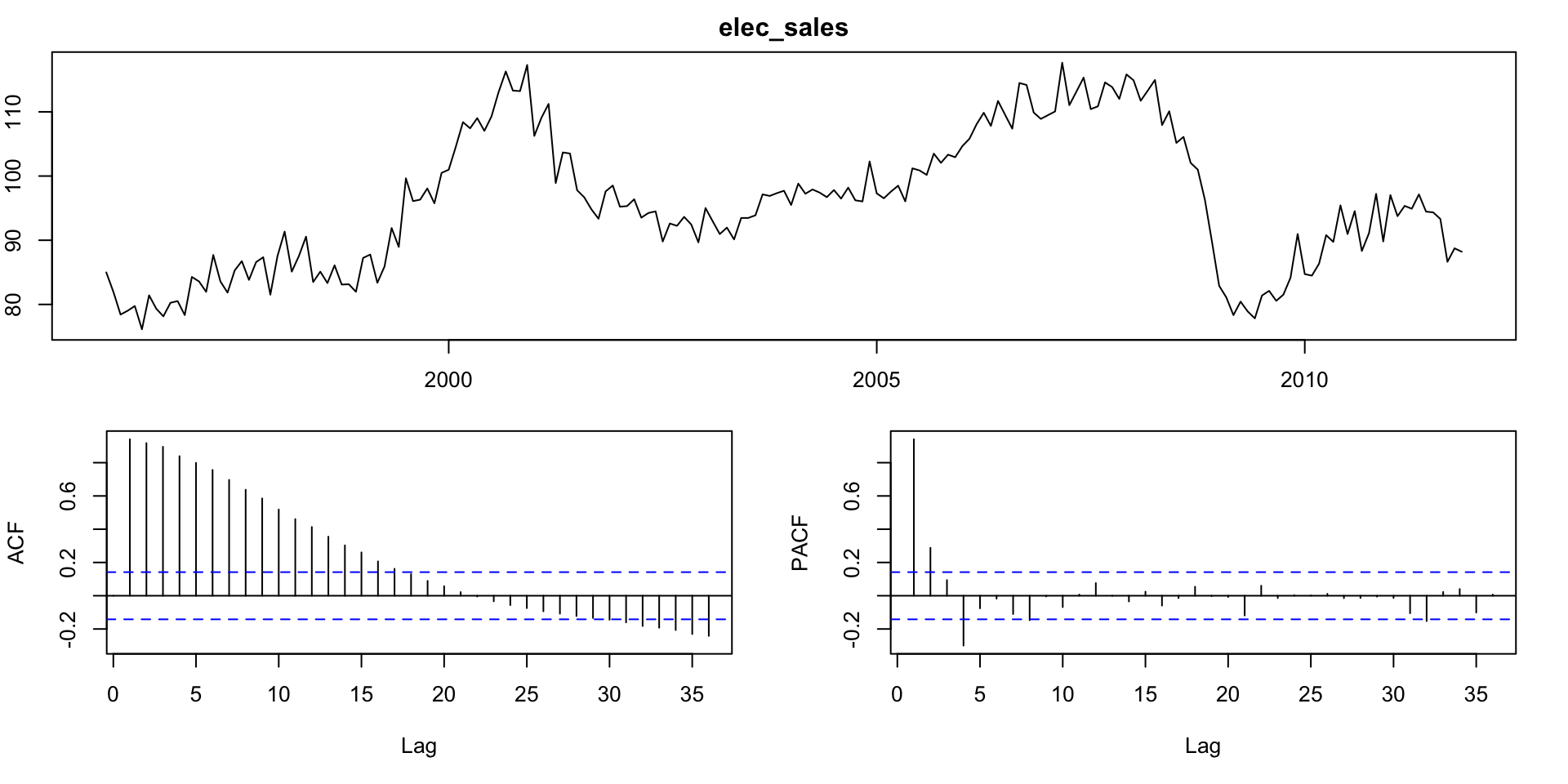

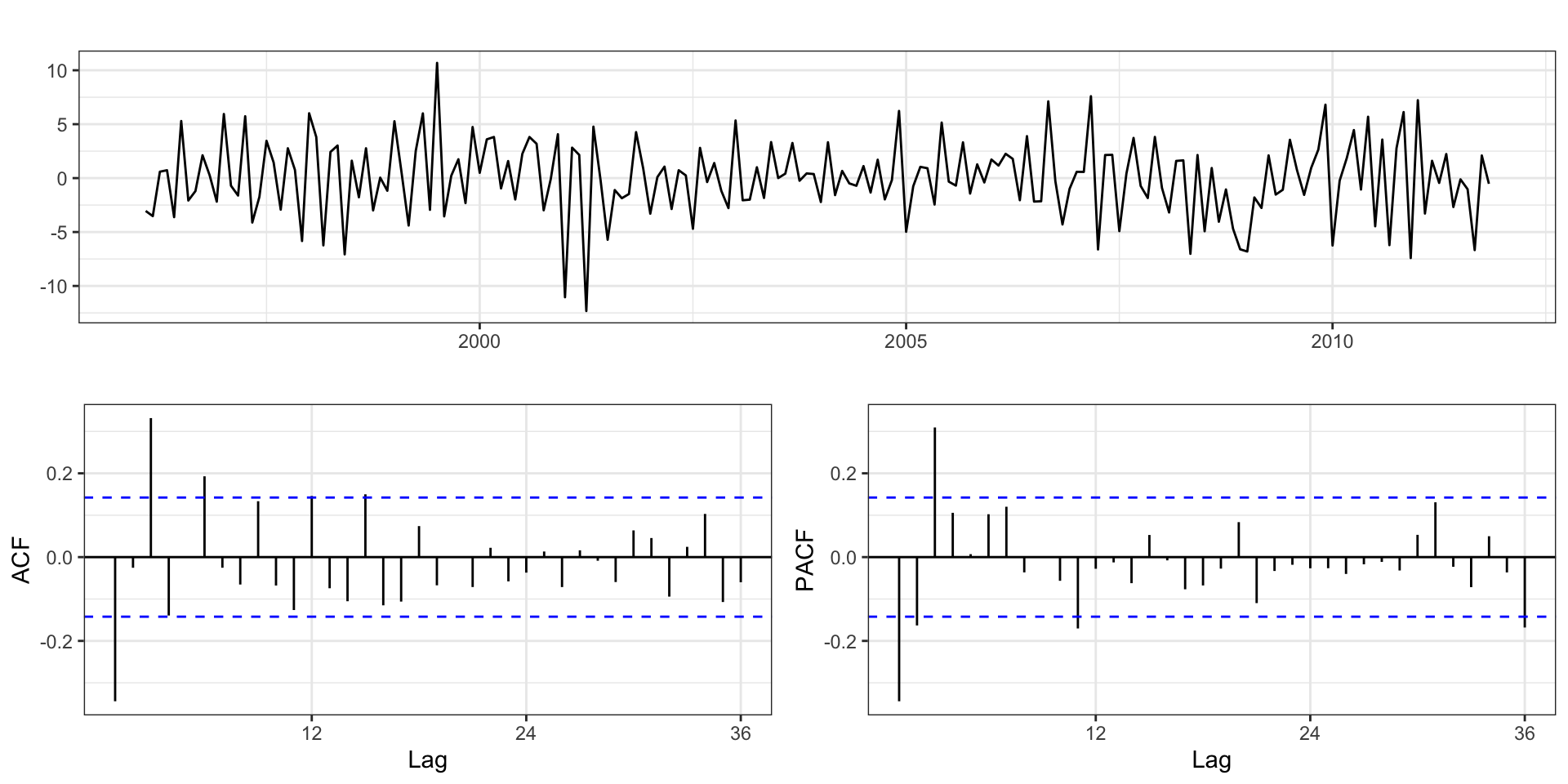

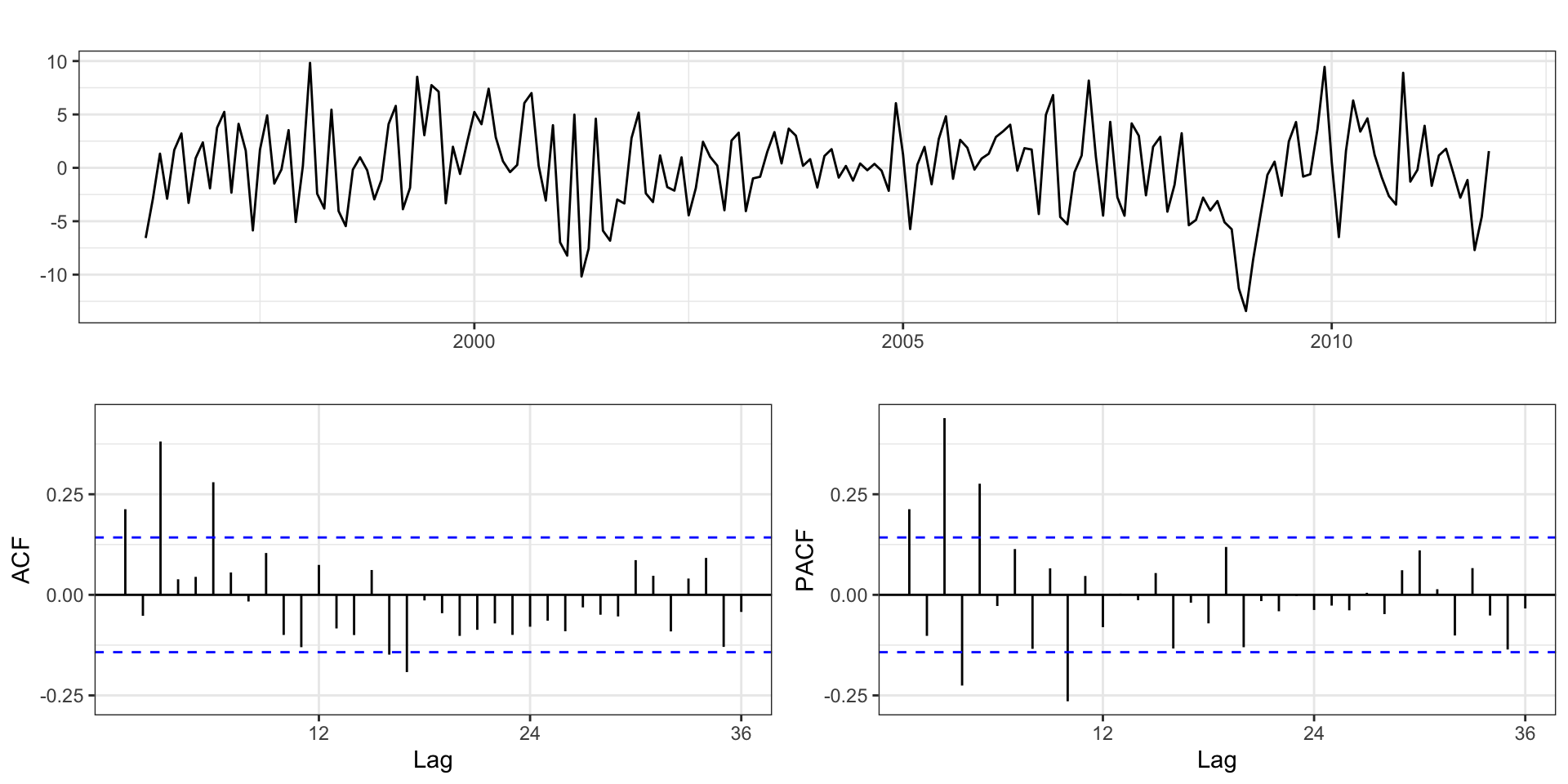

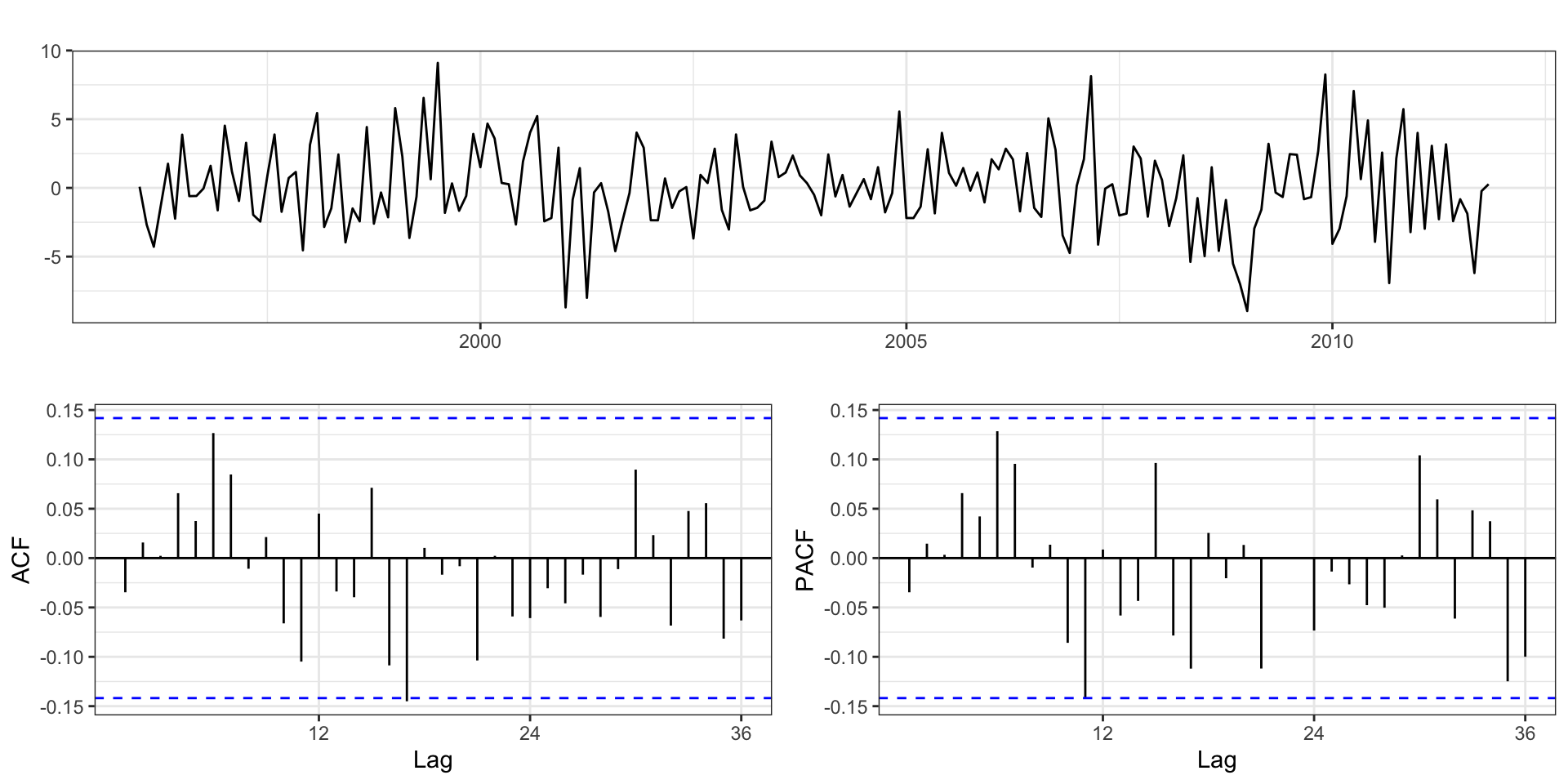

Differencing

Seasonal Arima

We can extend the existing ARIMA model to handle these higher order lags (without having to include all of the intervening lags).

Seasonal \(\text{ARIMA}\,(p,d,q) \times (P,D,Q)_s\) : \[ \Phi_P(L^s) \, \phi_p(L) \, \Delta_s^D \, \Delta^d \, y_t = \delta + \Theta_Q(L^s) \, \theta_q(L) \, w_t\] . . .

where

\[

\begin{aligned}

\phi_p(L) &= 1-\phi_1 L - \phi_2 L^2 - \ldots - \phi_p L^p\\

\theta_q(L) &= 1+\theta_1 L + \theta_2 L^2 + \ldots + \theta_p L^q \\

\Delta^d &= (1-L)^d\\

\\

\Phi_P(L^s) &= 1-\Phi_1 L^s - \Phi_2 L^{2s} - \ldots - \Phi_P L^{Ps} \\

\Theta_Q(L^s) &= 1+\Theta_1 L + \Theta_2 L^{2s} + \ldots + \theta_p L^{Qs} \\

\Delta_s^D &= (1-L^s)^D\\

\end{aligned}

\]

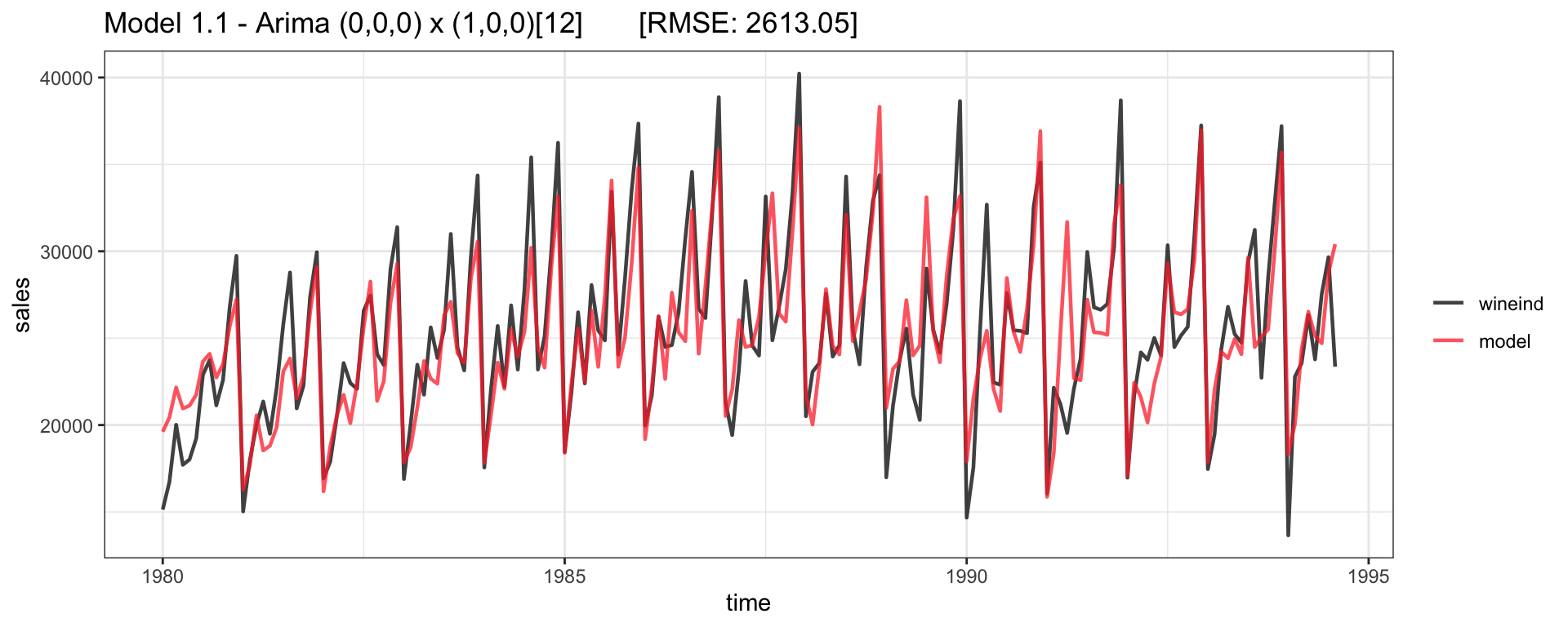

Seasonal ARIMA - AR

Lets consider an \(\text{ARIMA}(0,0,0) \times (1,0,0)_{12}\) : \[

\begin{aligned}

(1-\Phi_1 L^{12}) \, y_t = \delta + w_t \\

y_t = \Phi_1 y_{t-12} + \delta + w_t

\end{aligned}

\]

m1.1 = forecast:: Arima (wineind, seasonal= list (order= c (1 ,0 ,0 ), period= 12 )))

Series: wineind

ARIMA(0,0,0)(1,0,0)[12] with non-zero mean

Coefficients:

sar1 mean

0.8780 24489.243

s.e. 0.0314 1154.487

sigma^2 = 6906536: log likelihood = -1643.39

AIC=3292.78 AICc=3292.92 BIC=3302.29

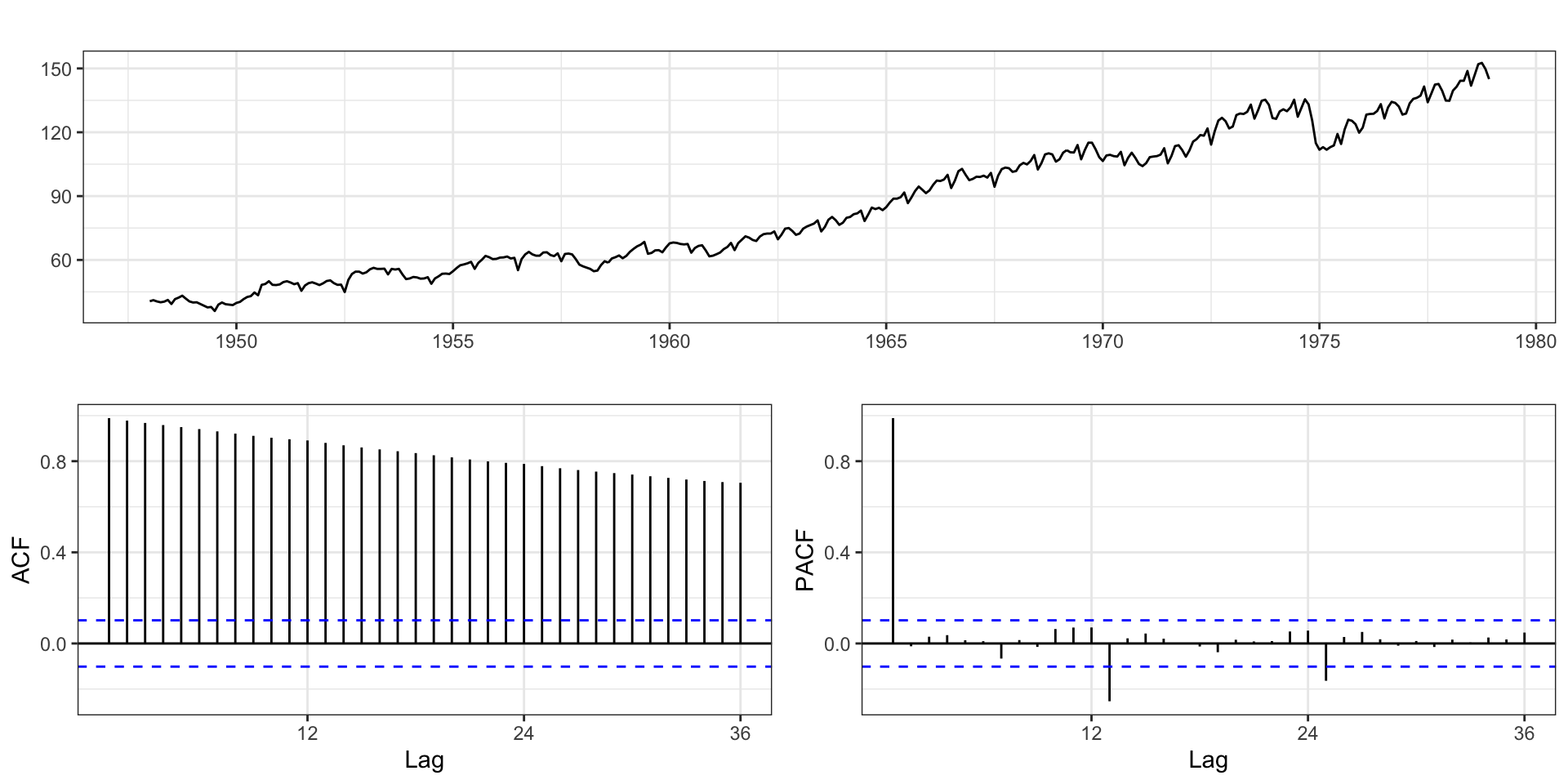

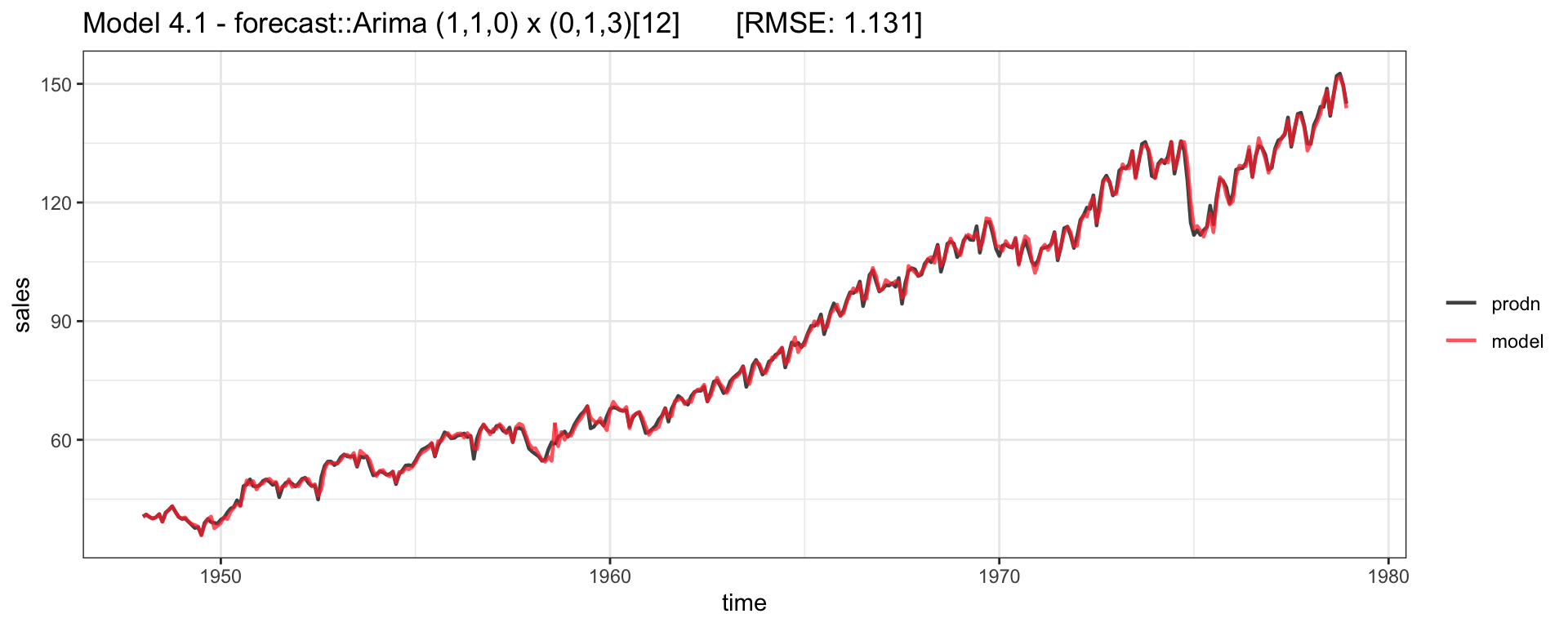

Fitted - Model 1.1

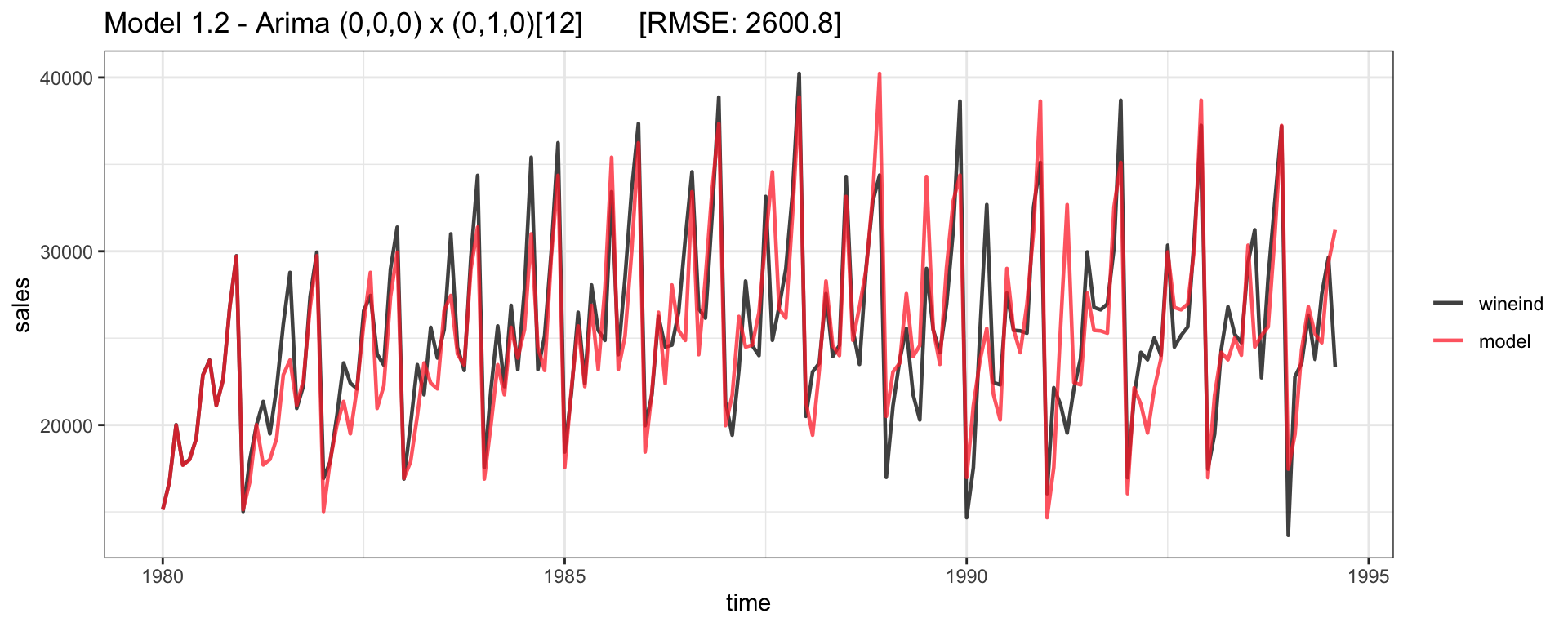

Seasonal Arima - Diff

Lets consider an \(\text{ARIMA}(0,0,0) \times (0,1,0)_{12}\) : \[

\begin{aligned}

(1 - L^{12}) \, y_t = \delta + w_t \\

y_t = y_{t-12} + \delta + w_t

\end{aligned}

\]

m1.2 = forecast:: Arima (seasonal= list (order= c (0 ,1 ,0 ), period= 12 )

Series: wineind

ARIMA(0,0,0)(0,1,0)[12]

sigma^2 = 7259076: log likelihood = -1528.12

AIC=3058.24 AICc=3058.27 BIC=3061.34

Fitted - Model 1.2

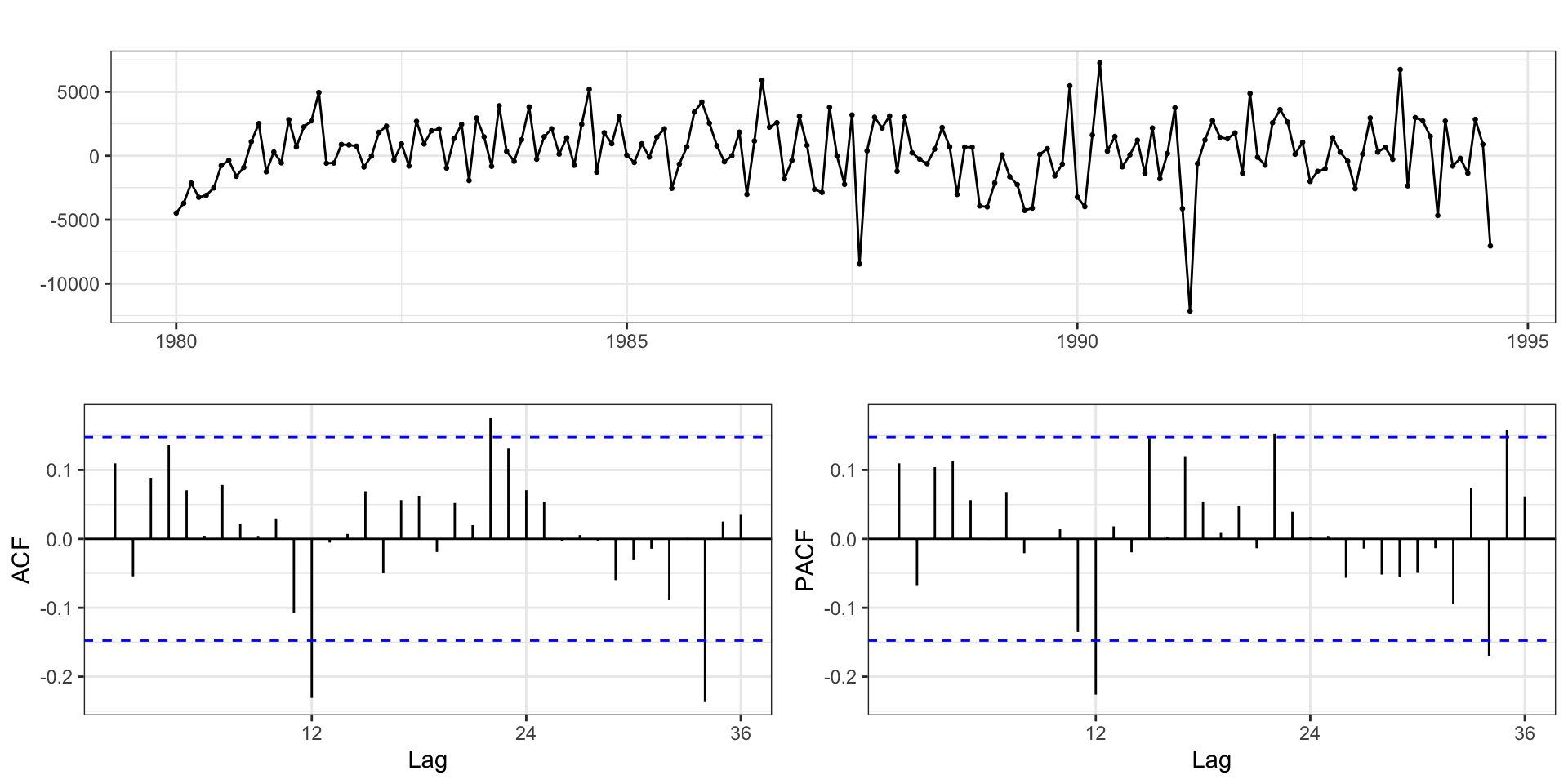

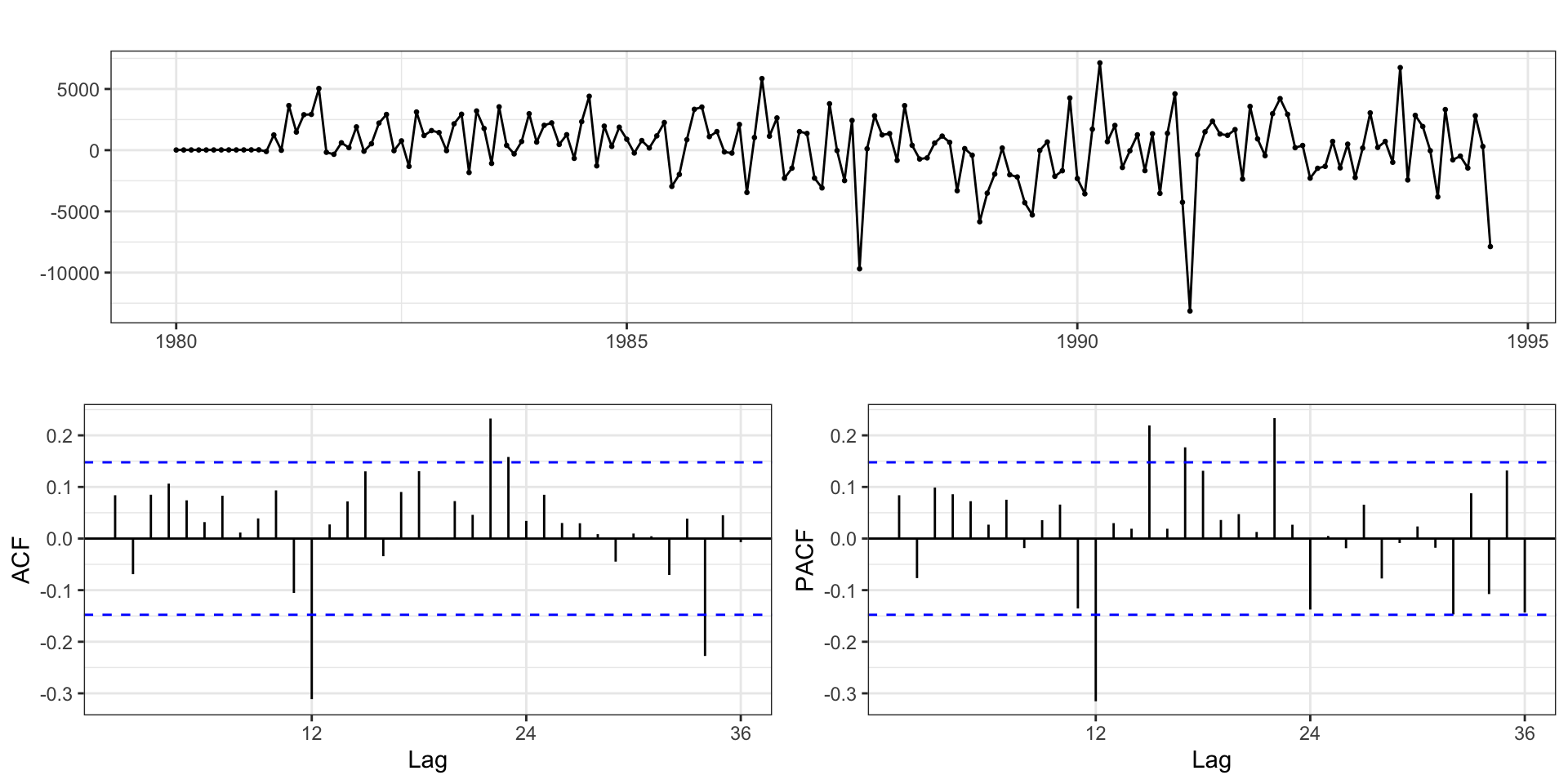

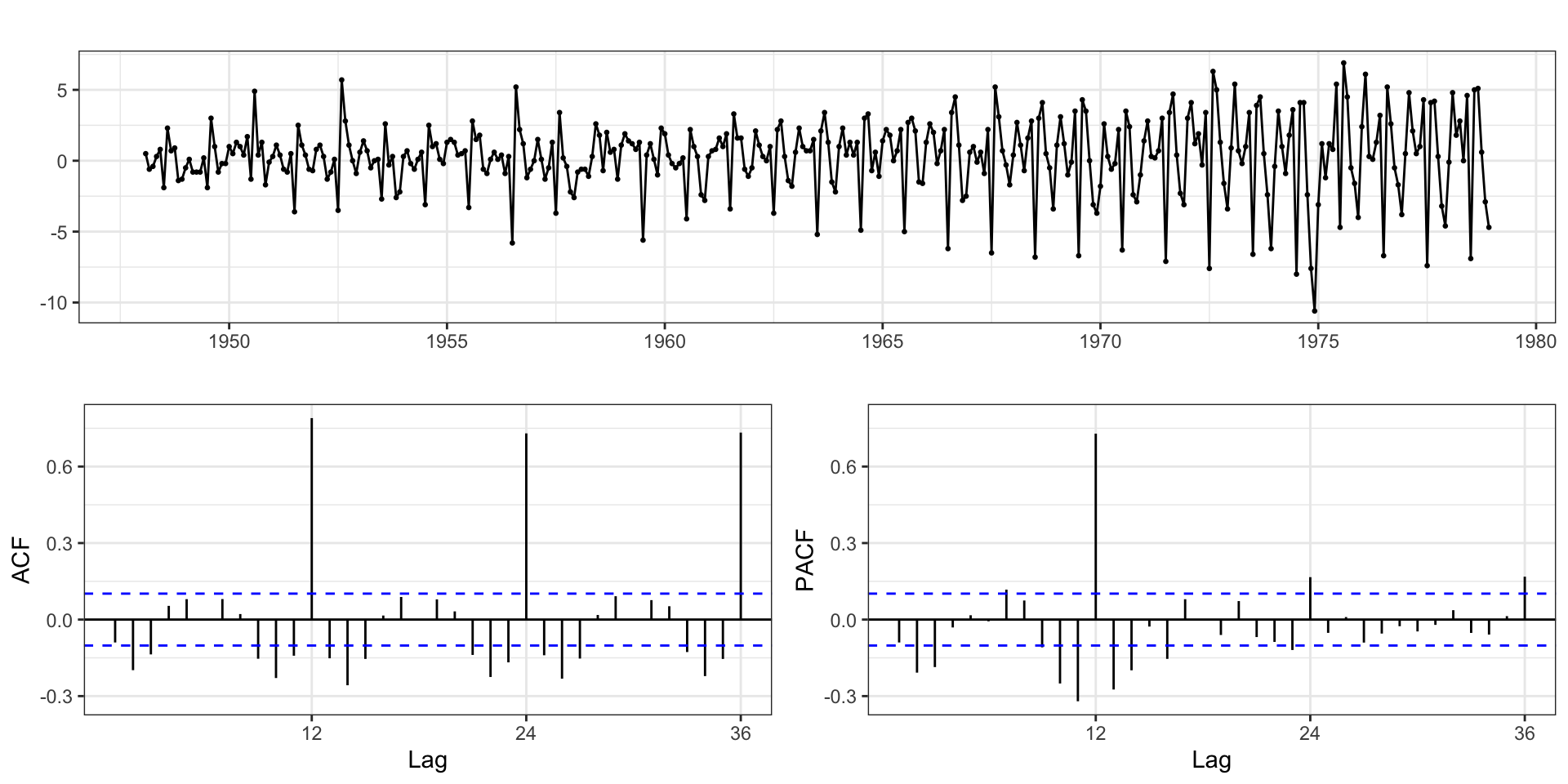

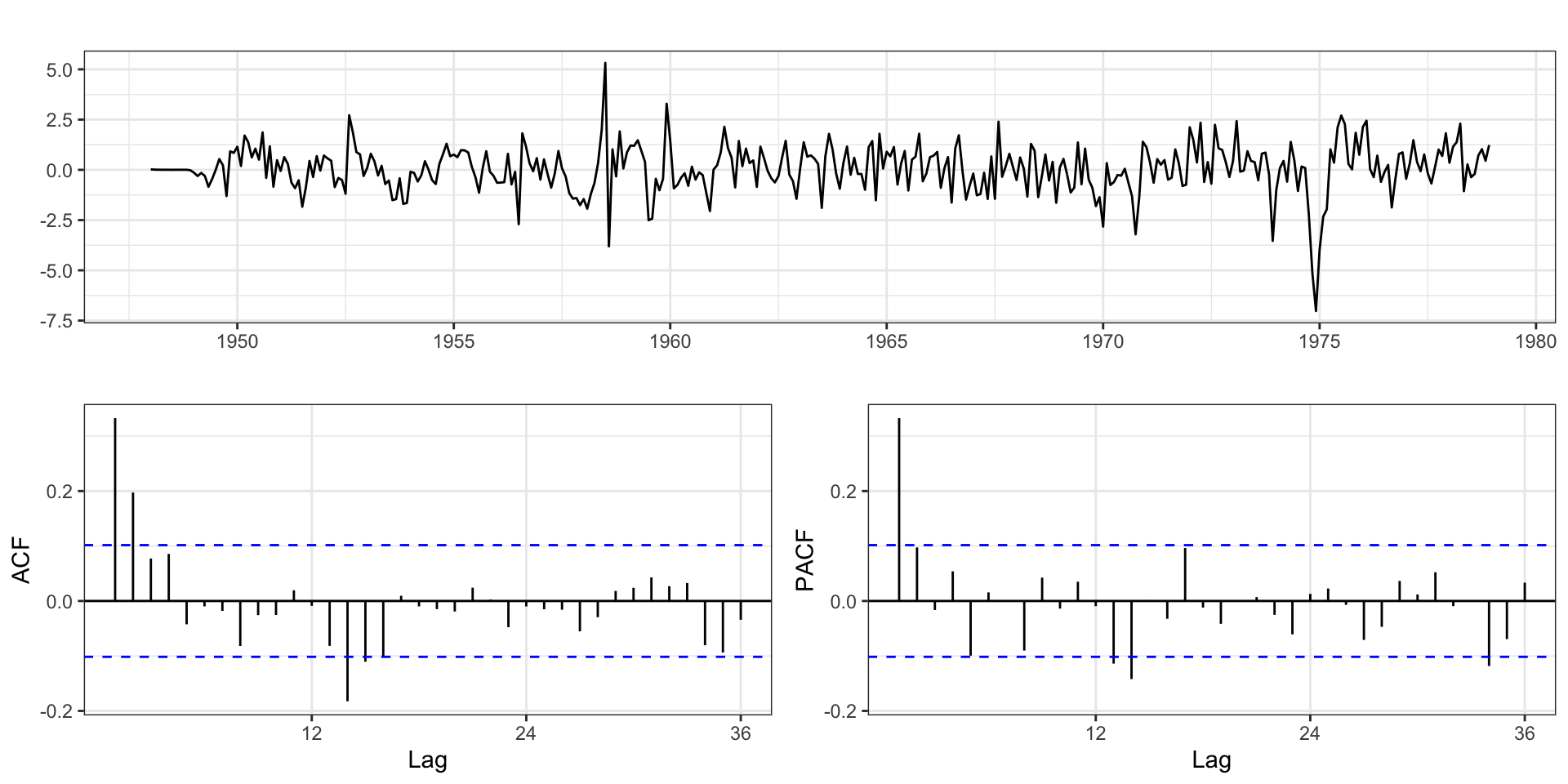

Residuals - Model 1.1 (SAR)

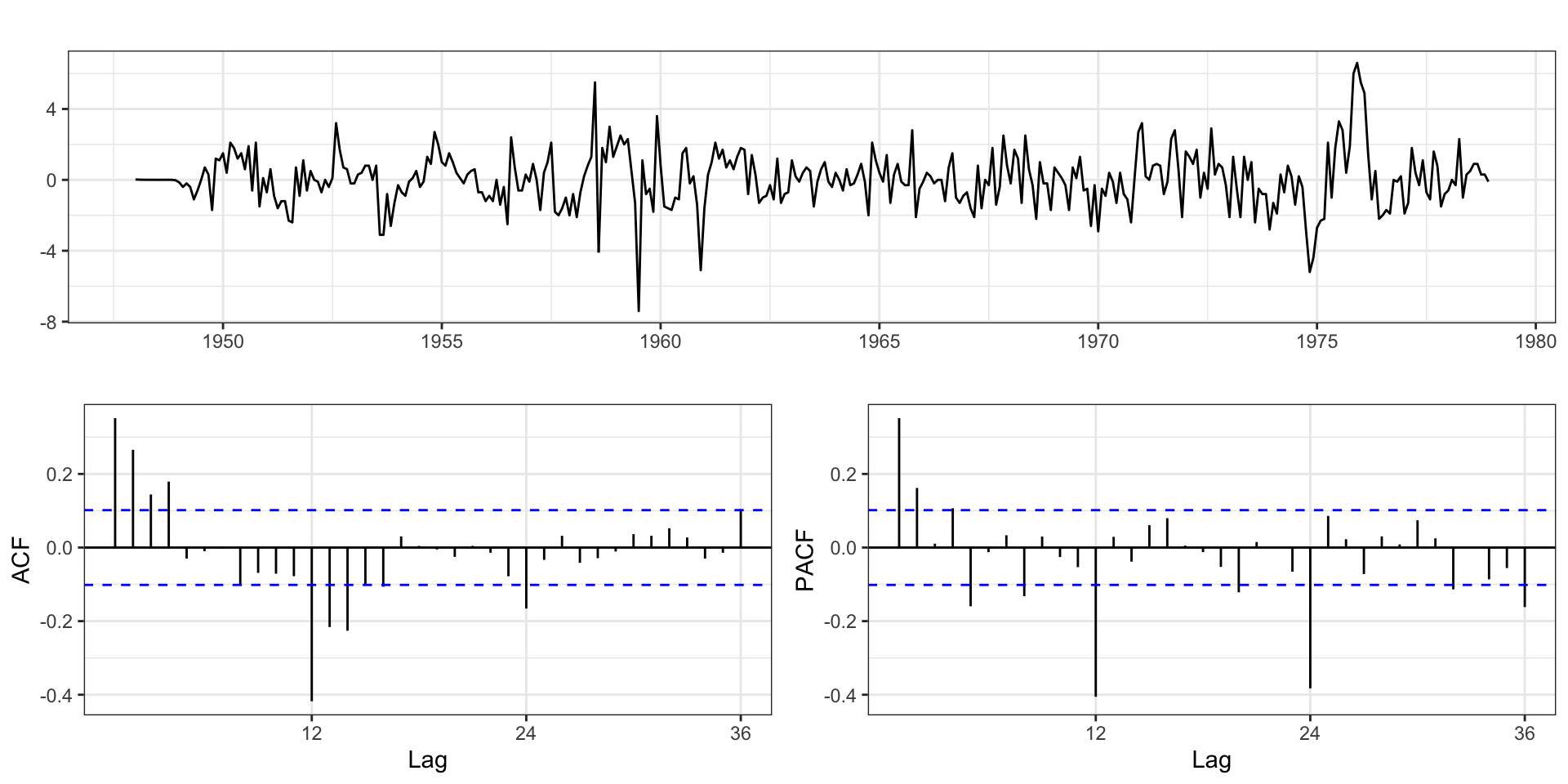

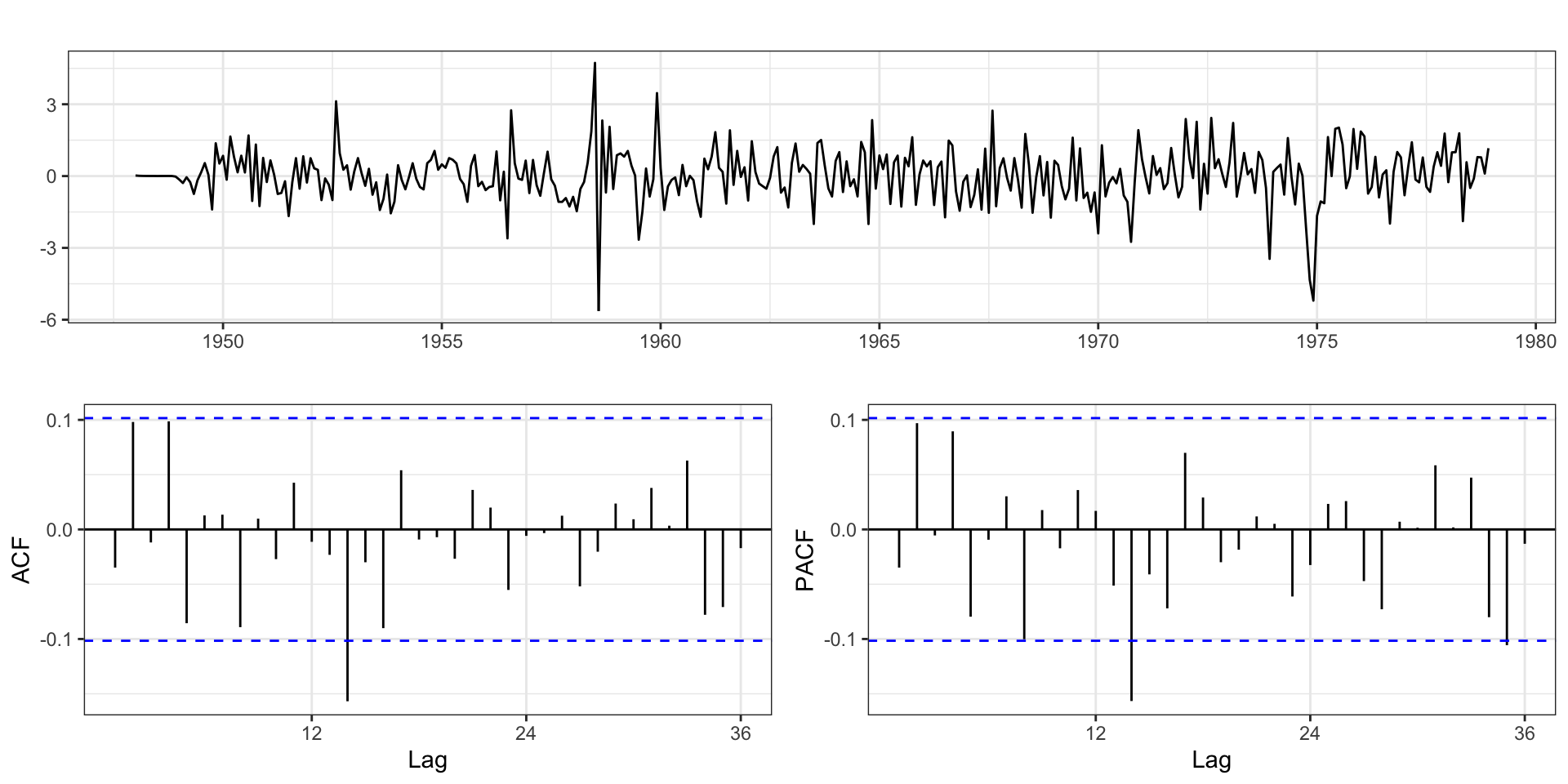

Residuals - Model 1.2 (SDiff)

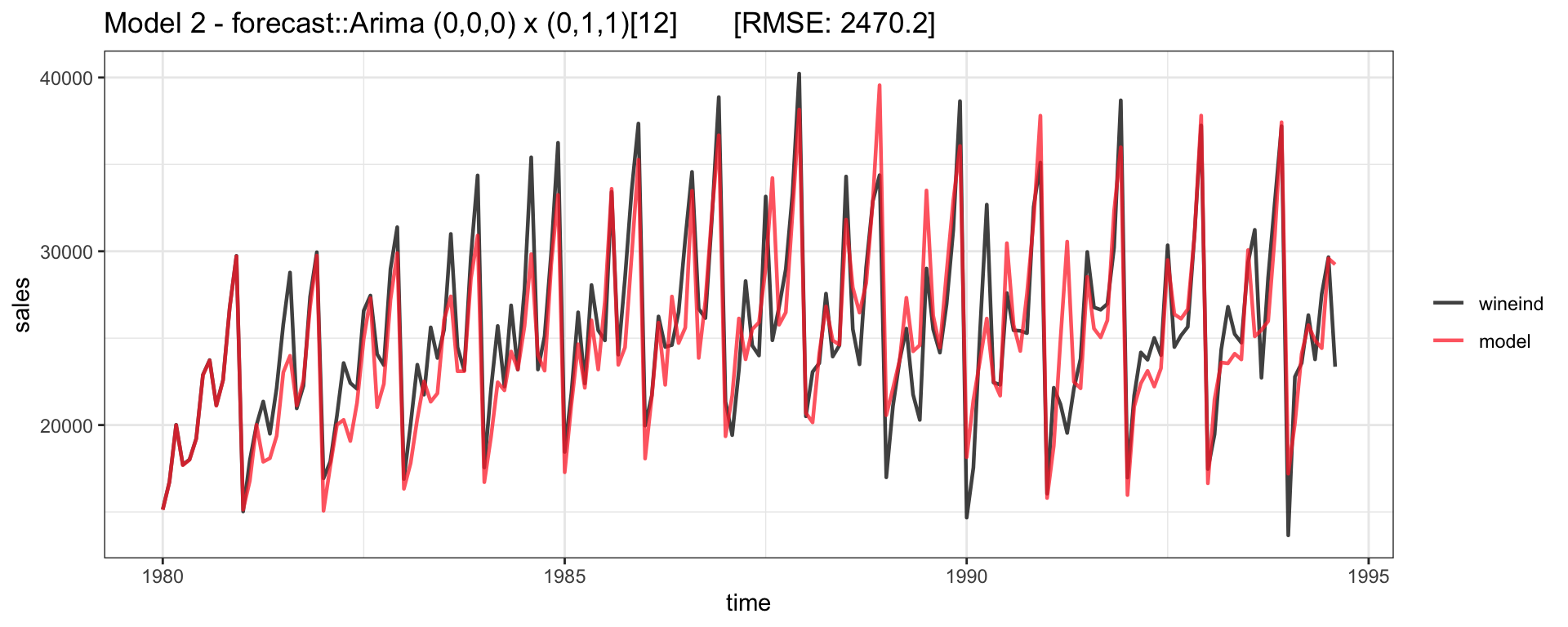

Model 2

\(\text{ARIMA}(0,0,0) \times (0,1,1)_{12}\) :

\[

\begin{aligned}

(1-L^{12}) y_t = \delta + (1+\Theta_1 L^{12}) w_t \\

y_t = \delta + y_{t-12} + w_t + \Theta_1 w_{t-12}

\end{aligned}

\]

m2 = forecast:: Arima (wineind, order= c (0 ,0 ,0 ), seasonal= list (order= c (0 ,1 ,1 ), period= 12 )))

Series: wineind

ARIMA(0,0,0)(0,1,1)[12]

Coefficients:

sma1

-0.3246

s.e. 0.0807

sigma^2 = 6588531: log likelihood = -1520.34

AIC=3044.68 AICc=3044.76 BIC=3050.88

Fitted - Model 2

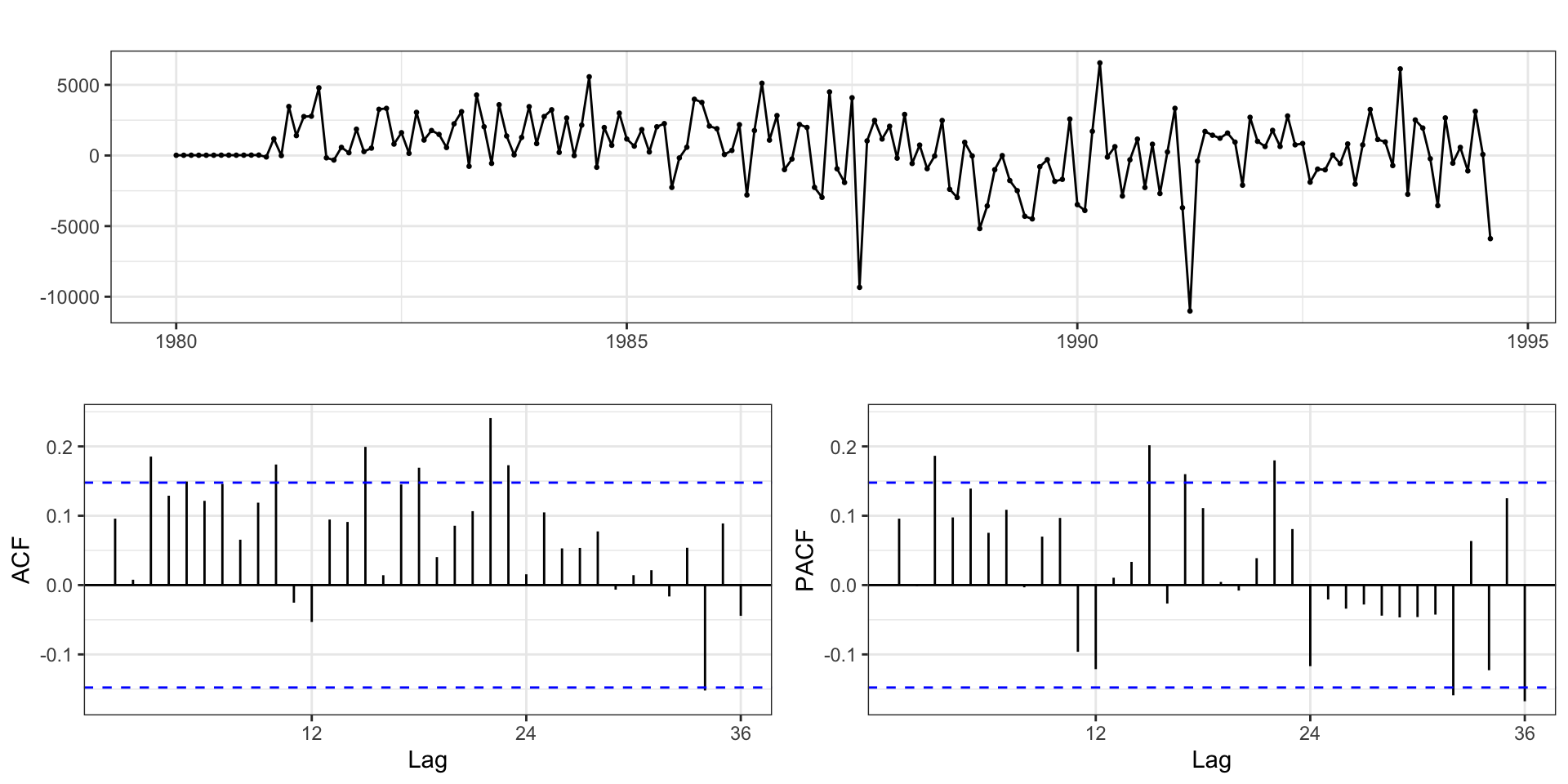

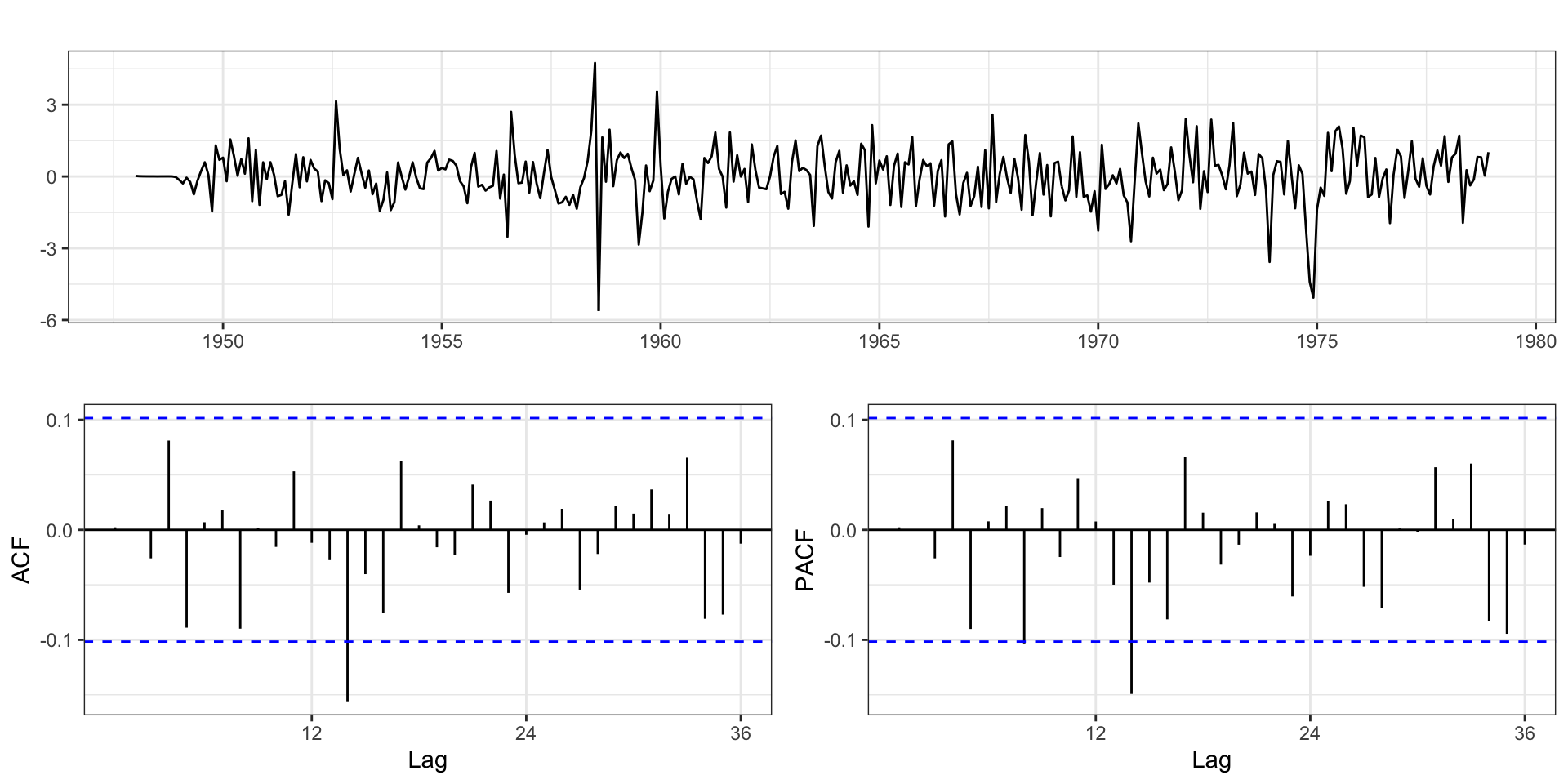

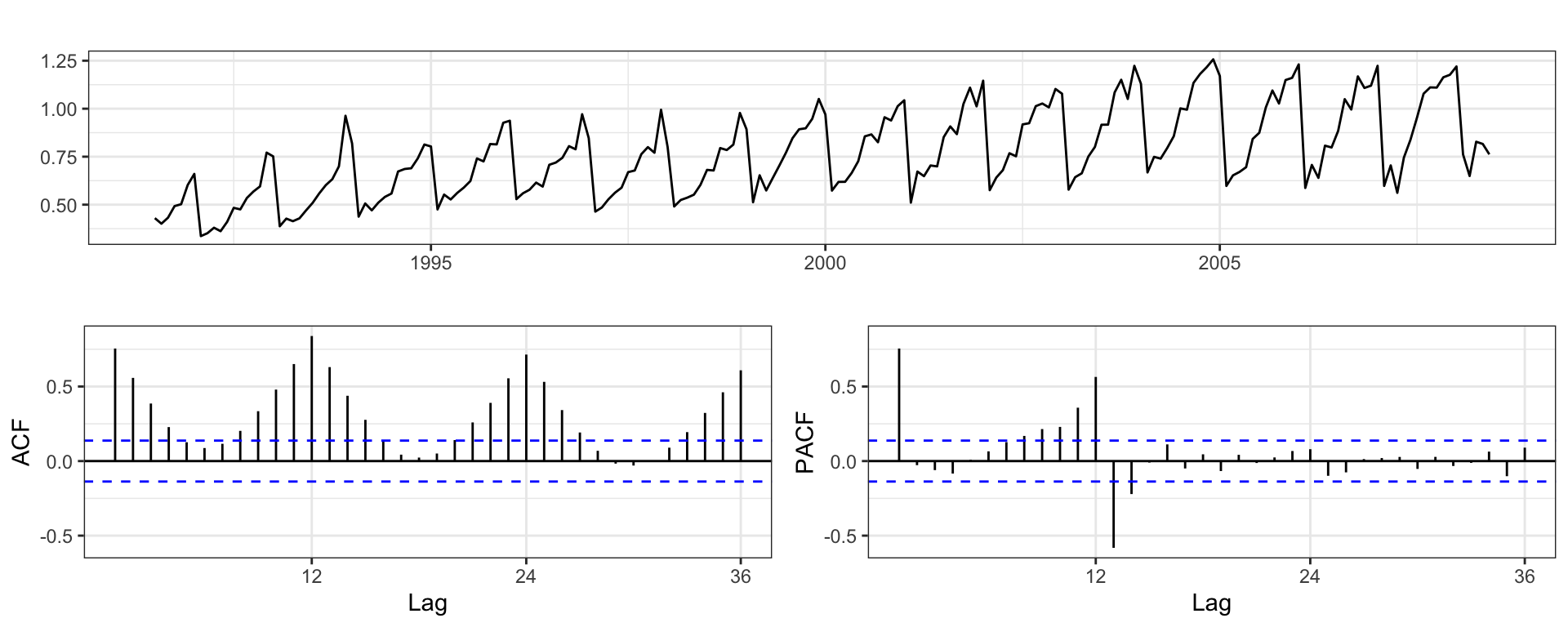

Residuals

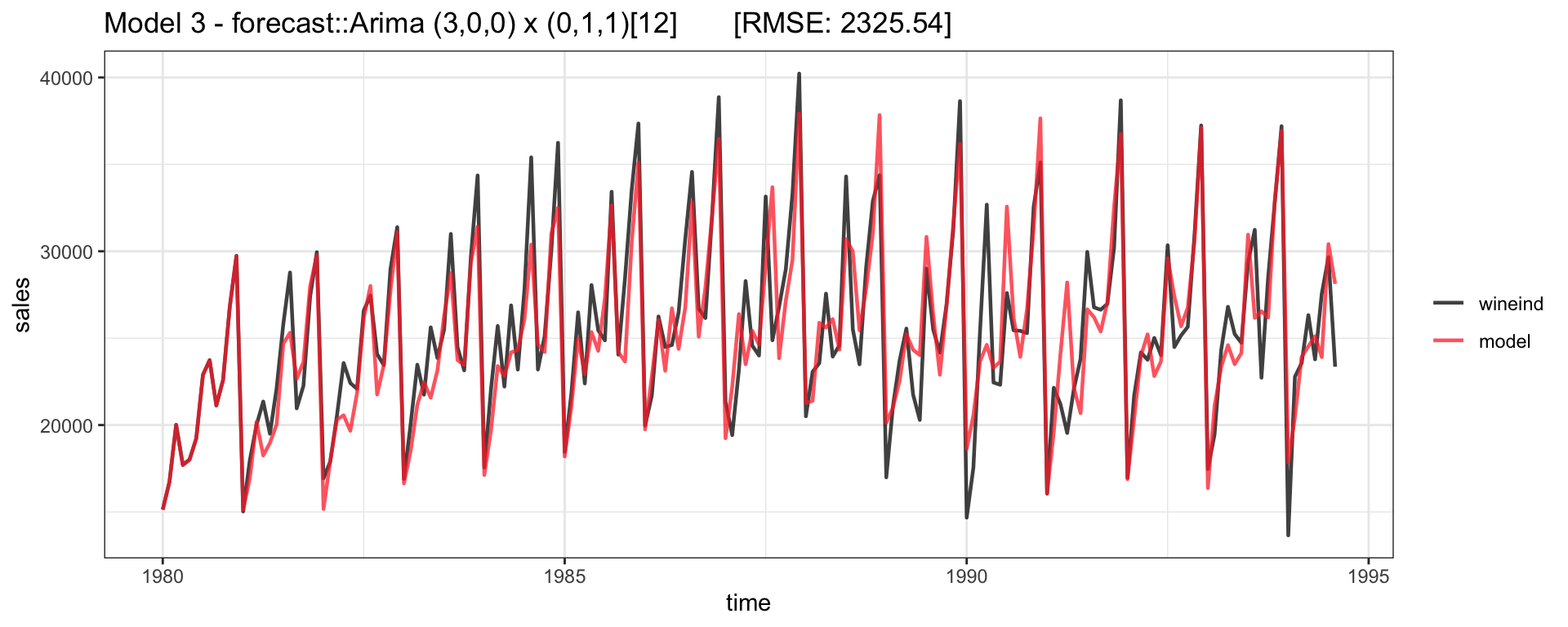

Model 3

\(\text{ARIMA}(3,0,0) \times (0,1,1)_{12}\)

\[

\begin{aligned}

(1-\phi_1 L - \phi_2 L^2 - \phi_3 L^3) \, (1-L^{12}) y_t = \delta + (1 + \Theta_1 L)w_t \\

y_t = \delta + \sum_{i=1}^3 \phi_i y_{t-i} + y_{t-12} - \sum_{i=1}^3 \phi_i y_{t-12-i} + w_t + w_{t-12}

\end{aligned}

\]

m3 = forecast:: Arima (wineind, order= c (3 ,0 ,0 ), seasonal= list (order= c (0 ,1 ,1 ), period= 12 )))

Series: wineind

ARIMA(3,0,0)(0,1,1)[12]

Coefficients:

ar1 ar2 ar3 sma1

0.1402 0.0806 0.3040 -0.5790

s.e. 0.0755 0.0813 0.0823 0.1023

sigma^2 = 5948935: log likelihood = -1512.38

AIC=3034.77 AICc=3035.15 BIC=3050.27

Fitted model

Model - Residuals